Pitfalls of Naive Portfolio Rebalancing

Rick Bookstaber and I discuss the pitfalls of naively using mean-variance optimization (MVO) when rebalancing portfolios to a target. We briefly touch upon the technique that I helped develop at Fabric called Guided Rebalancing.

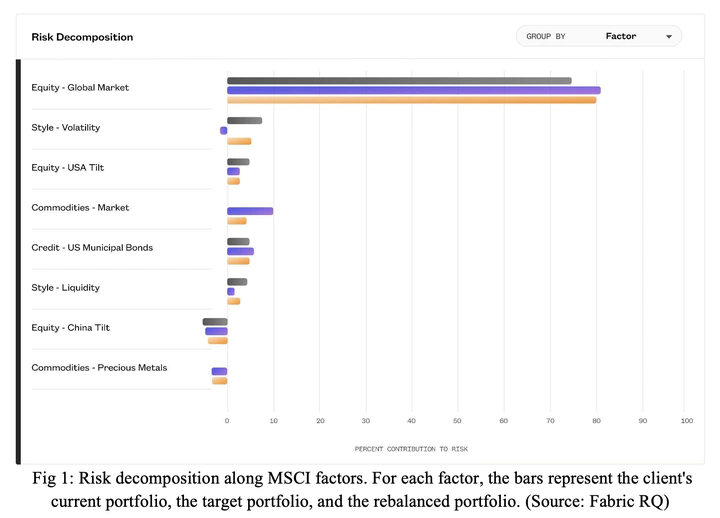

Guided Rebalancing uses factor risk contributions directly and in many ways circumvents many of the issues with MVO. The complete piece is available through Financial Advisor Magazine.

Dhruv Sharma

Researcher - Portfolio Construction, Risk Management, Agent-Based Models, Statistical Physics.

Physicist turned economic modeler trying to make sense of the world through ABMs.